What Is the Dutch Income Tax System?

Introduction

Understanding the Dutch income tax system in 2026 can feel overwhelming, especially with multiple tax boxes, changing rates, and various deductions. Whether you’re an expat, employee, or freelancer (ZZP), knowing how your income is taxed is essential to avoid overpaying and to make smarter financial decisions.

This guide breaks down everything into simple, structured, and easy-to-understand insights, so you can confidently navigate the Netherlands tax system.

What You’ll Learn in This Guide

In this complete guide, you’ll discover:

- How the Dutch income tax system works (Box 1, Box 2, Box 3 explained)

- Latest tax rates and changes for 2026

- Key deductions and tax credits available

- How freelancers (ZZP) and employees are taxed differently

- How the 30% ruling works for expats

- Real examples to simplify tax calculations

- Common mistakes and how to avoid them

- Answers to frequently asked tax-related questions

This guide is designed to give you clarity, confidence, and practical knowledge to manage your taxes effectively.

| Box | What it covers | 2026 rate |

|---|---|---|

| Box 1 | Income from employment, freelance work, pension, and own home | 35.75% – 49.50% |

| Box 2 | Income from a substantial interest (≥5% shareholding in a company) | 24.50% / 31% |

| Box 3 | Wealth from savings, investments, and other assets | 36% (on deemed return) |

Box 1 — Income from Work & Home (2026 Rates)

Box 1 is the most relevant category for the vast majority of people in the Netherlands. Since 2024, the Netherlands uses a three-bracket progressive system that creates a middle tier to differentiate lower and middle incomes while keeping the top rate unchanged at 49.50%.

| Bracket | Rate | Income Range | Notes |

|---|---|---|---|

| 1 | 35.75% | Up to €38,883 | Includes social security (AOW, Anw, Wlz) |

| 2 | 37.56% | €38,883 – €78,426 | Pure income tax (no social security) |

| 3 | 49.50% | Above €78,426 | Max deduction rate capped at 37.56% |

Special rates for AOW pension recipients

If you have reached state pension age (AOW-leeftijd), reduced rates apply in Bracket 1. For those born on or after 1 January 1946, the combined Bracket 1 rate is 17.85%. For those born before 1 January 1946, this lower rate applies to income up to €41,123.

Deduction rate cap for high earners

If your taxable income is €78,426 or above, be aware that personal deductions — including mortgage interest, the entrepreneur allowance, and the SME profit exemption — are capped at 37.56% (the second bracket rate), even though your marginal rate is 49.50%.

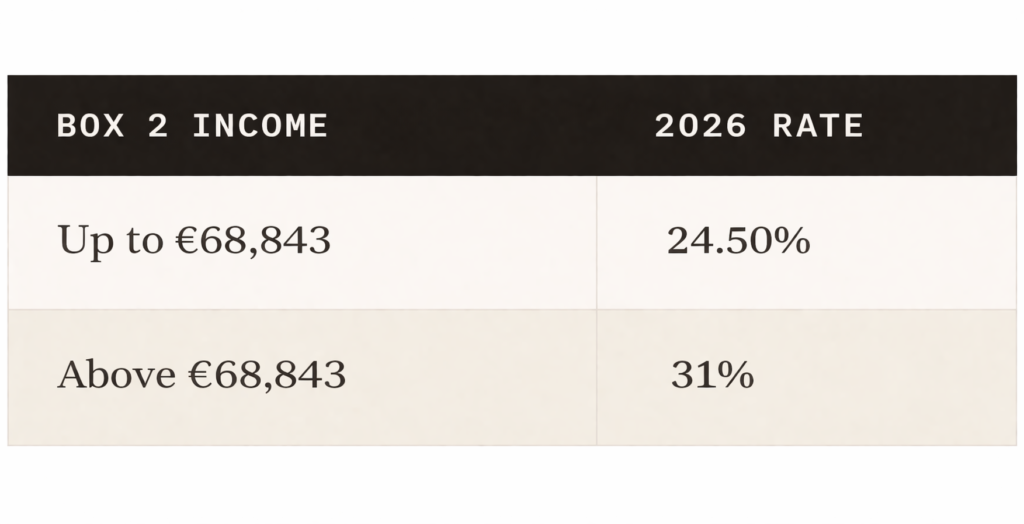

Box 2 — Substantial Business Interest

Box 2 applies if you and your fiscal partner together own at least 5% of the shares or voting rights in a company (BV, NV, or cooperative). This mainly affects director-major shareholders (DGAs) and business founders.

The lower bracket threshold increased by €1,039 from 2025, allowing slightly more income to benefit from the 24.5% rate. For fiscal partners, both can use the first bracket individually meaning a combined dividend can be more tax-efficient when split between partners.

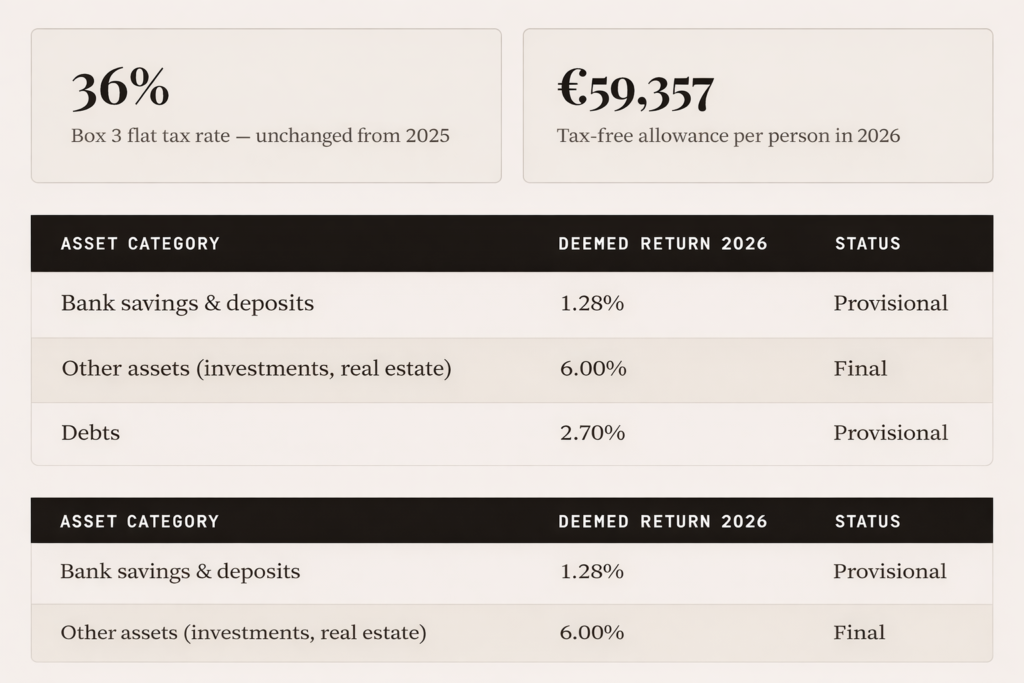

Box 3 — Wealth Tax on Savings & Investments

Box 3 is arguably the most debated part of Dutch tax law in recent years. Rather than taxing your actual returns, the Belastingdienst calculates a notional (deemed) return on your net assets above the tax-free threshold, then taxes that figure at a flat rate.

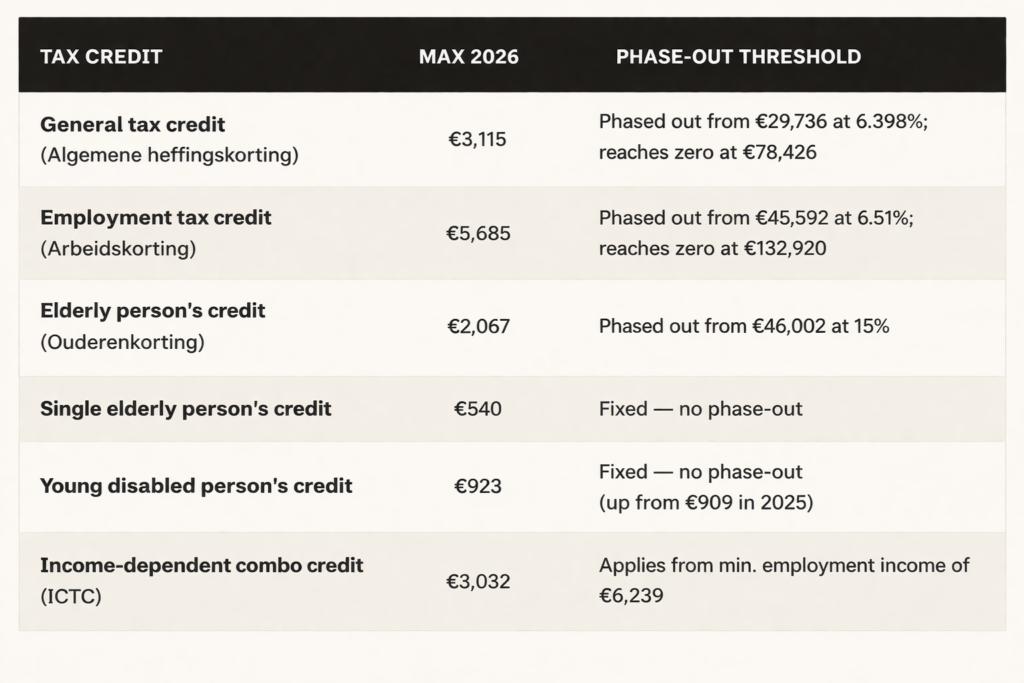

Key Tax Credits for 2026

Tax credits (heffingskortingen) directly reduce your tax liability and are more powerful than deductions. The two most impactful credits the general credit and the employment credit benefit the vast majority of Dutch taxpayers.

The general tax credit phases out completely at €78,426 aggregate income, meaning high earners receive no general credit. The employment credit disappears at €132,920 employment income.

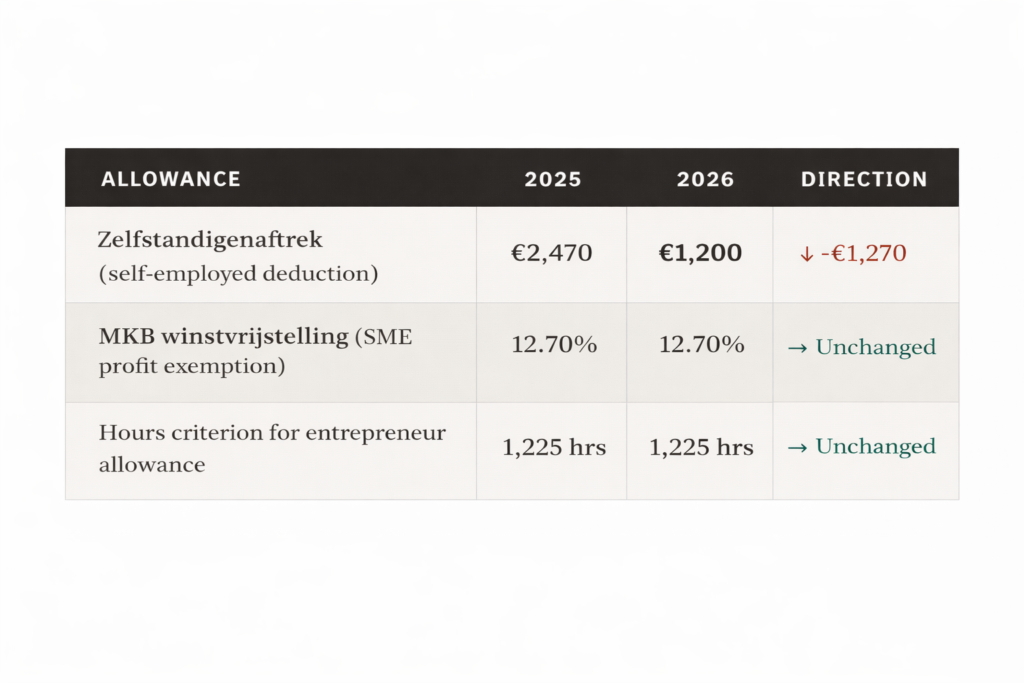

Tax Rules for Entrepreneurs & Freelancers in 2026

If you work as a ZZP’er (zelfstandige zonder personeel) or run a sole proprietorship (eenmanszaak) in the Netherlands, 2026 brings a significant financial change that raises the effective tax burden for most self-employed workers.

Key freelancer allowances at a glance

Running a BV? Corporate tax rates 2026

If you operate through a private limited company (BV), corporate income tax (vennootschapsbelasting) rates remain unchanged in 2026. The first bracket rate of 19% applies to taxable profits up to €200,000, and the top rate of 25.8% applies to profits above that.

Expats & the 30% Ruling in 2026

The 30% ruling (30%-regeling) is the Netherlands’ flagship benefit for attracting international talent. It allows qualifying employees to receive 30% of their gross salary as a tax-free expense reimbursement, dramatically reducing effective tax rates for high-earning expats.

What changed in 2026

The extraterritorial cost reimbursement scheme (ETK regeling) has been tightened. Two previously deductible categories have been abolished from 2026: additional costs of living (gas, water, electricity, and other utilities), and the costs of non-business phone calls to your home country. If you currently rely on these deductions, contact your employer or tax advisor to review your compensation package.

2025 vs 2026 — What Actually Changed?

Here is a side-by-side overview of all the key changes between the 2025 and 2026 Dutch tax years, so you can quickly identify what directly affects your situation.

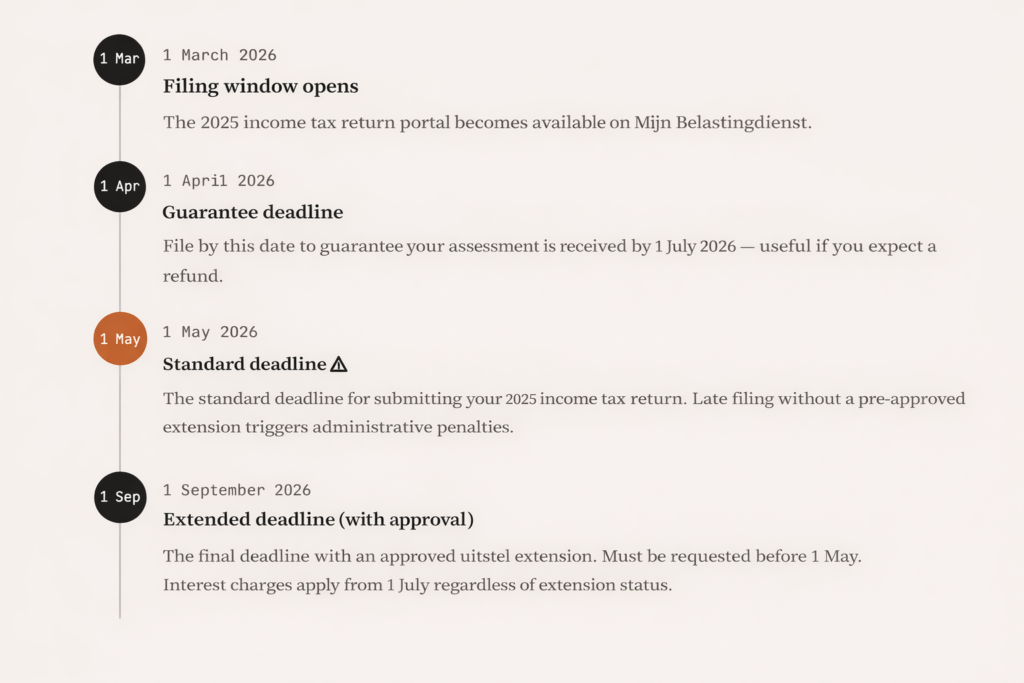

Filing Deadlines & How to File Your Dutch Tax Return

The Dutch tax year follows the calendar year: 1 January to 31 December. Your 2026 income tax return (for the 2025 tax year) must be filed according to the following key dates:

How to file

Dutch residents file their annual tax return (aangifte inkomstenbelasting) through one of the following: online via Mijn Belastingdienst (Dutch-language portal, requires DigiD), through a registered tax advisor or accountant (belastingadviseur), or using DigiD-compatible tax software. If you arrived in or left the Netherlands during 2025, you typically need to file an M-form (migration year return) rather than the standard return.

Frequently Asked Questions – Dutch Income Tax 2026

The following questions are structured to target Google’s People Also Ask boxes and Featured Snippets for the keyword “Dutch income tax 2026“. Click each question to expand the answer.

What are the Dutch income tax rates for 2026?

In 2026, Dutch income tax (Box 1) uses three brackets: income up to €38,883 is taxed at 35.75%, income between €38,883 and €78,426 is taxed at 37.56%, and income above €78,426 is taxed at the top rate of 49.50%. The Bracket 1 rate includes social security premiums. Brackets 2 and 3 are pure income tax.

What is the tax-free allowance in the Netherlands for 2026?

The Netherlands does not use a single personal tax-free income allowance. Instead, tax credits reduce your bill directly. The maximum general tax credit is €3,115 and the maximum employment tax credit is €5,685 in 2026. For Box 3 wealth, the tax-free exemption is €59,357 per person.

When is the Dutch income tax return deadline in 2026?

The filing window for 2025 income tax returns opens on 1 March 2026. The standard deadline is 1 May 2026. With a pre-approved extension (uitstel), the final deadline is 1 September 2026. Filing late without approval results in administrative penalties, and interest begins accruing from 1 July 2026 regardless.

What is the top income tax rate in the Netherlands in 2026?

The top income tax rate in the Netherlands is 49.50% in 2026, applying to Box 1 income above €78,426. Note that personal deductions such as mortgage interest and entrepreneur allowances are capped at the second bracket rate of 37.56% for high earners, not the top rate.

How does the Dutch Box 3 wealth tax work in 2026?

Box 3 taxes a notional (deemed) return on your net assets at a flat rate of 36%. The tax-free allowance is €59,357 per person. The deemed return is 6.0% for investments and other assets, and 1.28% (provisional) for bank savings in 2026. If your actual return was lower, you can dispute the assessment using the OWR form (Opgaaf Werkelijk Rendement).

John Keller is the founder of Look Forward Administratie & Advies and a Dutch financial administration and tax advisory specialist. With 25 years of experience helping expats, freelancers, and businesses navigate Dutch payroll, income tax, and the 30% ruling, he combines hands-on advisory experience with a focus on making Dutch tax rules understandable for non-Dutch speakers.