VAT Refund Guide Netherlands 2026: How to Claim Back Dutch VAT

The Netherlands introduced major VAT refund rule changes in 2026 including mandatory digital portals, higher invoice thresholds, and new accommodation VAT rates. This guide covers everything you need to claim Dutch VAT back correctly this year.

What You’ll Learn in This Guide

In this complete VAT refund guide for the Netherlands (2026), you’ll discover:

- Latest VAT rule changes and updates for 2026

- Current Dutch VAT rates and when they apply

- Different types of VAT refunds (business, EU, travel, etc.)

- Step-by-step VAT refund process (BTW Teruggaaf)

- Eligibility criteria and required documents

- Common mistakes that delay or reject refunds

- Practical tips to maximize your VAT claims

- Answers to frequently asked VAT-related questions

This guide is designed to give you clear understanding + actionable steps so you can claim your VAT refund correctly and efficiently.

1. What’s New in 2026 – Key Changes You Must Know

The Netherlands has rolled out several significant VAT changes effective January 1, 2026, and April 1, 2026. If you are claiming Dutch VAT refunds this year under any category, these updates directly affect your process and deadlines.

| Change | Effective Date | Who Is Affected | Status |

|---|---|---|---|

| Non-EU VAT refunds must be filed online only (13th Directive — via Mijn Belastingdienst Zakelijk with DigiD/eHerkenning) | April 1, 2026 | Non-EU businesses | Major Change |

| Tourist VAT refund goes fully digital — retailers must register purchases via MijnDouane; paper invoices/stamps no longer accepted | January 1, 2026 (paper allowed until March 31 for pre-2025 purchases) | Non-EU tourists & retailers | Major Change |

| Invoice attachment mandatory for EU/non-EU cross-border VAT refund claims over €1,000 (or €250 for fuel) | January 1, 2026 (invoices required in portal from April 1) | EU & non-EU foreign businesses | New Rule |

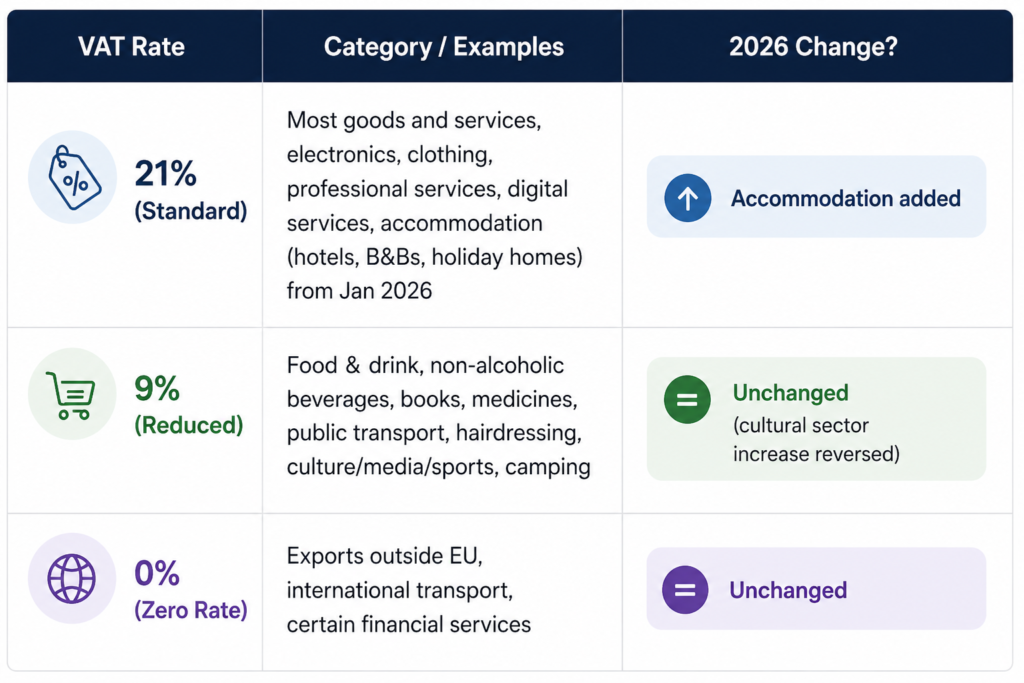

| Accommodation VAT rises from 9% to 21% — hotels, B&Bs, holiday homes, Airbnb-style rentals | January 1, 2026 | Hospitality businesses & travelers | Rate Change |

| Culture, media & sports VAT stays at 9% — planned increase to 21% was reversed by parliament | Cultural sector businesses | Reversal | |

| Objections against nil VAT returns eliminated — a nil return is now legally treated as a payment | January 1, 2026 | VAT-registered Dutch businesses | Procedural Change |

Paper submissions rejected from April 1, 2026Non-EU businesses that submit paper VAT refund claims after April 1, 2026 will have those claims rejected or returned unprocessed by the Belastingdienst. Portal registration (DigiD or eHerkenning) can take several weeks – if you haven’t registered yet, treat this as urgent.

2. Dutch VAT Rates 2026

The Netherlands operates three VAT (BTW) tiers. The 2026 Dutch Tax Plan introduced one significant rate change – accommodation services -while reversing a proposed change for cultural services.

Accommodation booking transitional ruleIf you booked and paid for accommodation in 2025 but the stay falls in 2026, the 21% rate still applies. This is a transitional rule under the 2026 Tax Plan. Only camping stays remain at 9%.

3. Types of VAT Refunds in the Netherlands

There are four main routes for claiming Dutch VAT back, each with different eligibility rules, procedures, and 2026-specific requirements:

🇳🇱 Dutch-Registered Businesses

- Claim via regular BTW return (monthly/quarterly)

- Automatic refund if input VAT exceeds output VAT

- Electronic filing mandatory

- Fastest route — 2–3 weeks for refund

🇪🇺 EU Businesses (8th Directive)

- For EU businesses not VAT-registered in NL

- Submit via home country’s online portal

- Deadline: September 30 of following year

- Invoice attachment required for claims >€1,000

Non-EU Businesses (13th Directive)

- From April 2026: online portal only

- Requires DigiD or eHerkenning access

- Reciprocity agreement required

- Minimum €430 for annual claim

Non-EU Tourists

- Fully digital from January 2026

- Use ‘NL Customs VAT’ app to claim

- Minimum €50 per receipt

- Must export goods within 3 months

4. Business VAT Refund (BTW Teruggaaf) – For Dutch-Registered Businesses

If your business is VAT-registered in the Netherlands, claiming input VAT back is part of your standard VAT return process through the Belastingdienst. This is the most straightforward route and results in refunds within 2–3 weeks of submission.

Filing Frequency

- Monthly – if your annual turnover exceeds €1.883 million

- Quarterly – if annual turnover is below €1.883 million

- Annually – only with advance permission from the Belastingdienst (strict conditions apply)

2026 Filing Deadlines to NoteVAT returns are due by the last day of the month following the reporting period. In 2026, certain deadlines fall on weekends – including January, April, and September periods — so payment must reach the Belastingdienst by the last working day before the deadline. Late payments may incur penalties.

What VAT Can You Claim Back?

- Business purchases from suppliers with valid invoices (VAT number shown)

- Import VAT on goods entering the Netherlands

- Professional services used for business purposes

- Business travel and accommodation (note: accommodation now at 21% VAT in 2026)

- Office supplies, equipment, machinery

- Marketing and advertising expenses

What VAT Cannot Be Claimed?

- Personal or private expenses mixed with business costs

- Entertainment expenses (with limited exceptions)

- Company cars – partial restrictions apply based on business use percentage

- Domestic accommodation (hotels for personal use)

5. EU Business VAT Refund (8th Directive / Cross-Border)

EU businesses that are VAT-registered in their home country but not registered in the Netherlands can reclaim Dutch VAT through the 8th Directive cross-border mechanism. This process runs through your home country’s online VAT portal.

Eligibility Requirements

- Business is established and VAT-registered in another EU member state

- Not VAT-registered in the Netherlands

- Paid Dutch VAT on genuine business expenses during the claim period

- Invoices show Dutch VAT (BTW) amount clearly

2026 New Requirement: Invoice Attachment

From January 1, 2026 onwards, EU businesses must attach invoices and import documents when the claim per invoice exceeds€1,000, or€250 for fuel. Claims without required attachments will not be processed from April 1, 2026.

Application Steps

- Log in to your home country’s VAT portal

Each EU country has its own online portal. In Germany, this is ELSTER; in France, impots.gouv.fr, etc. - Select the Netherlands as the refund country

You will be directed or redirected to the correct cross-border claim section. - Upload invoices for amounts over €1,000

This is a new 2026 requirement. Invoices below this threshold remain optional but recommended. - Submit by September 30 of the following year

Claims for 2025 Dutch VAT must be submitted by September 30, 2026. - Track your claim

The Belastingdienst processes standard claims within 4 months. Complex or incomplete cases can take up to 8 months.

| Parameter | Rule |

|---|---|

| Minimum claim (annual) | €400 |

| Minimum per invoice | €50 |

| Invoice attachment required | Yes, if claim per invoice > €1,000 (or €250 for fuel) from 2026 |

| Submission deadline (2025 claims) | September 30, 2026 |

| Standard processing time | 4 months |

| Extended processing time | Up to 8 months |

6. Non-EU Business VAT Refund (13th Directive) – 2026 Portal Rules

This is the most significantly changed area for 2026. Non-EU businesses that have paid Dutch VAT most commonly on imports routed through Rotterdam can reclaim it under the 13th Directive. But the entire procedure has shifted from paper-based to digital-only.

From April 1, 2026 — Online Portal OnlyThe Belastingdienst has discontinued paper submissions for the 13th Directive procedure. From the second calendar quarter of 2026, all non-EU VAT refund requests must be submitted throughMijn Belastingdienst Zakelijk. Access requires either DigiD(for natural persons) oreHerkenning(for companies). Both processes can take several weeks to obtain — start immediately if you haven’t already.

How to Access the Portal

- Determine your login method

Natural persons use DigiD. Legal entities (companies) use eHerkenning. The required level depends on your business type check belastingdienst.nl/business-login. - Apply for eHerkenning or DigiD access

This is a separate registration process that can take several weeks. Non-resident businesses often need to engage a local Dutch agent or intermediary who already has portal access. - Register as a foreign entrepreneur

If you don’t yet have a Dutch registration number, use the Registration form for Foreign Companies first. Don’t attach invoices to this form. - File your VAT refund claim via the portal

Submit through Mijn Belastingdienst Zakelijk with all supporting documentation including invoices for claims over €1,000.

Eligible Non-EU Countries (2026)

The Netherlands maintains reciprocity agreements – your country must offer comparable VAT refund rights to Dutch businesses:

| Country | Reciprocity Status |

|---|---|

| 🇺🇸 United States | Full reciprocity |

| 🇨🇭 Switzerland | Full reciprocity |

| 🇳🇴 Norway | Full reciprocity |

| 🇯🇵 Japan | Full reciprocity |

| 🇦🇺 Australia | Full reciprocity |

| 🇨🇦 Canada | Full reciprocity |

| 🇰🇷 South Korea | Full reciprocity |

Minimum Claim Thresholds (13th Directive)

- €430 minimum for a full calendar year claim

- €130 minimum for shorter periods

- €50 minimum per individual invoice

7. Tourist VAT Refund – Now Fully Digital in 2026

Non-EU tourists visiting the Netherlands can reclaim the VAT (BTW) paid on purchases they take home. As of 2026, this process is now entirely digital – the old paper Tax Free Form system with physical stamps has been discontinued.

New in 2026: ‘NL Customs VAT’ AppTourists now use the‘NL Customs VAT’ app(available in multiple languages) to apply for their VAT refund. Retailers must register purchases digitally via MijnDouane or through an approved intermediary. Paper invoices and stamps are no longer valid for purchases made after December 31, 2025. (Transitional period: purchases made before December 31, 2025 could still use paper until March 31, 2026.)

Eligibility for Tourist VAT Refund

- You must be a permanent resident outside the European Union

- Purchases must be at least €50 per receipt (per retailer)

- Goods must be exported out of the EU within 3 months of purchase

- Purchases must be physical goods you take with you — services don’t qualify

New Digital Process – Step by Step

- Shop at a participating Dutch retailer

Ask the retailer to register your purchase digitally via MijnDouane using your passport details. Not all retailers participate – ask in advance. - Download the ‘NL Customs VAT’ app

Available for iOS and Android in multiple languages. This app is your digital tax-free voucher. - At the border/airport before departure

Show your goods to Dutch Customs for verification. Customs stamps your claim digitally in the app. - Receive your refund

The refund is processed through the retailer’s appointed refund operator — via bank transfer, card credit, or at an airport refund desk. Service fees of 2–4% typically apply.

Refund Rates for Tourists

- Items at 21% standard rate: up to 17.4% effective refund (after service fees)

- Items at 9% reduced rate: up to 7.4% effective refund

- Service/handling fees: typically 2–4% deducted by refund operators

8. Documentation Requirements 2026

Documentation rules have tightened in 2026. Having incorrect or incomplete records is the single biggest reason VAT refund claims are rejected.

What a Valid Dutch VAT Invoice Must Include

- Supplier’s full name and address

- Supplier’s VAT (BTW) registration number

- Invoice date and unique invoice number

- Your business name and address

- Detailed description of goods or services supplied

- Net amount (excluding VAT), VAT percentage applied, and VAT amount clearly stated

- Total amount including VAT

Additional Documents by Claim Type

| Claim Type | Required Supporting Documents |

|---|---|

| Dutch-registered business | Original VAT invoices, proof of payment, import documents where applicable |

| EU cross-border (8th Directive) | VAT invoices (mandatory for >€1,000 per invoice from 2026), home-country VAT registration certificate, bank details |

| Non-EU business (13th Directive) | Original invoices, certificate of entrepreneurship from home tax authority, proof of payment, portal login (DigiD/eHerkenning from April 2026) |

| Tourist | Passport, digital purchase registration via MijnDouane, ‘NL Customs VAT’ app, goods for inspection at customs |

9. Key Deadlines & Timeline 2026

2026 VAT Refund Deadlines at a Glance

March 31, 2026Last date for paper tourist VAT refunds (pre-2025 purchases)

April 1, 2026Non-EU 13th Directive claims: online portal only (paper rejected)

September 30, 2026Deadline for EU cross-border claims (8th Directive) for 2025 Dutch VAT

June 30, 2026 (approx.)Non-EU 13th Directive: typical deadline for prior year claims (confirm with Belastingdienst)

Monthly / QuarterlyDutch-registered businesses: last day of month following reporting period

4-year lookbackMaximum period for retrospective non-EU VAT claims

10. Common Mistakes – and How to Avoid Them in 2026

Most Common Reasons for Rejection

- Continuing to use paper submissions after April 1, 2026 — non-EU claims submitted on paper will be rejected entirely

- Missing invoice attachments — from 2026, invoices over €1,000 must be attached; omitting them means automatic rejection

- Not having DigiD or eHerkenning — non-EU businesses without portal access cannot file at all. Apply well in advance

- Late submissions — the September 30 deadline for EU cross-border claims is absolute; no extensions granted

- Claiming personal or mixed-use expenses — accommodation, meals, and travel must be evidenced as business-related

- Invalid invoice format — missing supplier VAT number or absent VAT amount breakdown invalidates the claim

- Claiming in the wrong category — EU businesses cannot use 13th Directive; non-EU businesses cannot use the EU 8th Directive portal

Best Practices for 2026

- Register for DigiD or eHerkenning immediately if you are a non-EU business processing can take several weeks

- Retain all Dutch VAT invoices digitally, organized by date and supplier

- Flag all invoices over €1,000 and ensure supporting documents are ready for attachment

- Engage a Dutch tax agent or intermediary if portal access is proving difficult

- For tourists: always ask retailers if they participate in the new digital scheme before purchasing

- Track claim status proactively — contact the Belastingdienst if you receive no decision within 4 months

Pro Tip: Rotterdam Import VATNon-EU sellers who route goods through Rotterdam generate Dutch import VAT at 21% on the customs value. For every €100,000 of customs value, that’s up to €21,000 of potentially refundable Dutch import VAT. Given the 2026 portal-only rule, ensuring portal access before the April 1 deadline is a high-value compliance action.

{FAQ}

How long do Dutch VAT refunds take in 2026?

Dutch-registered businesses receiving electronic refunds typically see funds within 2–3 weeks of a processed return. EU businesses using the 8th Directive should expect 4 months for standard claims, and up to 8 months if the Belastingdienst requests additional information. Non-EU 13th Directive claims have a similar processing window of 4–8 months via the new online portal.

I’m a non-EU business and don’t have DigiD or eHerkenning. What should I do?

Start the registration process immediately – both processes can take several weeks and you need portal access before April 1, 2026. Alternatively, engage a Dutch resident tax agent or intermediary who already has access and can file on your behalf. Without valid portal access, your claim cannot be submitted from Q2 2026 onwards.

Can I still claim VAT on hotel stays in the Netherlands in 2026?

Yes – businesses can still claim input VAT on genuine business accommodation. However, be aware that hotel, B&B, and similar accommodation VAT has risen from 9% to 21% from January 1, 2026. This doesn’t prevent reclaiming it, but the invoices will show the higher 21% rate. Only camping stays remain at 9%.

What is the minimum VAT amount I can claim back?

It depends on your category: EU cross-border (8th Directive) – €400 minimum for a full calendar year, €50 per invoice. Non-EU (13th Directive) – €430 for an annual claim, €130 for shorter periods, €50 per invoice. Tourists need a minimum of €50 per retailer receipt. Dutch-registered businesses have no minimum threshold.

Can I claim VAT on company car expenses?

Partial VAT recovery is possible for company cars depending on the percentage of business use. For a car used 100% for business, full input VAT may be recoverable. Mixed private/business use requires a proportional approach. Fuel costs under the VAT system have a separate €250 threshold for invoice attachment from 2026.

© 2026 DutchTaxCalculators.com

This VAT refund guide is for informational purposes only and does not constitute professional tax advice.

Always verify details with the official Belastingdienst (Dutch Tax Authority).

Need help? Use our Dutch VAT Calculator to estimate your refund instantly.

John Keller is a passionate entrepreneur and trusted business advisor dedicated to helping companies grow with clarity, structure, and confidence. With years of experience in business administration, financial management and strategic advisory, he works closely with entrepreneurs to create practical solutions tailored to their unique goals and challenges.

At Look Forward Administratie & Advies, the focus goes beyond numbers and administration. John believes that every successful business starts with clear insight and a strong strategy. By simplifying financial processes and providing real-time business insights, he helps entrepreneurs stay focused on what they do best while building a solid foundation for future growth.

Known for his personal approach and forward-thinking mindset, John supports businesses not only administratively but also as a coach and strategic partner. His mission is to help entrepreneurs recognize opportunities, overcome challenges and achieve long-term success with confidence.