Commissioner of Income Tax in the Netherlands

Table Of Content

What Is a Commissioner of Income Tax?

A Commissioner of Income Tax is a senior tax authority responsible for overseeing income tax administration, enforcing tax laws, handling disputes, and ensuring taxpayer compliance within a defined jurisdiction.

In the Netherlands, this function is carried out through the Belastingdienst, the Dutch Tax and Customs Administration which operates under the Ministry of Finance. Rather than using a single “Commissioner” title, the Dutch system distributes these responsibilities across a structured hierarchy of tax inspectors (belastinginspecteurs), regional directors, and the Director-General of the Belastingdienst.

Whether you are an employee, expat, freelancer, or business owner living in the Netherlands, understanding how the Dutch income tax authority works and what powers it holds can help you navigate assessments, resolve disputes, and stay fully compliant.

How the Dutch Tax Authority Is Structured

The Belastingdienst employs over 28,000 staff and is one of the largest government agencies in the Netherlands. Its structure determines who handles your tax matters at each stage:

| Level | Role |

| Ministry of Finance | Sets national tax policy and legislation |

| Director-General (DG) | Heads the entire Belastingdienst |

| Regional Director | Oversees a geographic tax region |

| Tax Inspector (Belastinginspecteur) | Assesses, audits, and decides on individual tax cases |

| Tax Officer | Handles day-to-day filing, payments, and queries |

The Tax Inspector is the Dutch equivalent of what many countries call a Commissioner of Income Tax; they hold legal authority to assess your income, issue additional tax demands, conduct audits, and rule on formal objections.

What Does the Dutch Commissioner of Income Tax (Tax Inspector) Do?

The Tax Inspector at the Belastingdienst performs four core functions:

1. Assessing Income Tax

The Tax Inspector reviews income tax returns filed through Mijn Belastingdienst (the personal tax portal) and issues a final tax assessment (aanslag). This assessment confirms how much income tax you owe or how much you will receive as a refund based on your declared income across Box 1, Box 2, and Box 3.

If you have not filed a return, the Tax Inspector is authorised to issue an ex officio assessment (ambtshalve aanslag), estimating your tax liability based on available financial data.

2. Conducting Tax Audits

Tax inspectors may request any information and documentation relevant to your tax position, interview you as the taxpayer, and assess the accuracy of your reported information. Taxpayers are legally obligated to provide this information within a specified timeframe.

Audits can be triggered randomly or based on specific risk signals such as unexplained income, discrepancies in reported assets, or sector-wide compliance checks.

3. Issuing Additional Tax Assessments

If the Tax Inspector believes that the initial assessment is incorrect, an additional assessment (naheffingsaanslag) can be issued with or without penalties and interest, depending on the reason for underpayment.

4. Deciding on Formal Objections

When a taxpayer disagrees with a tax assessment, the Tax Inspector reviews the formal objection (bezwaar) and issues a revised decision.The Tax Administration will usually issue a decision within 6 weeks after receiving your objection.

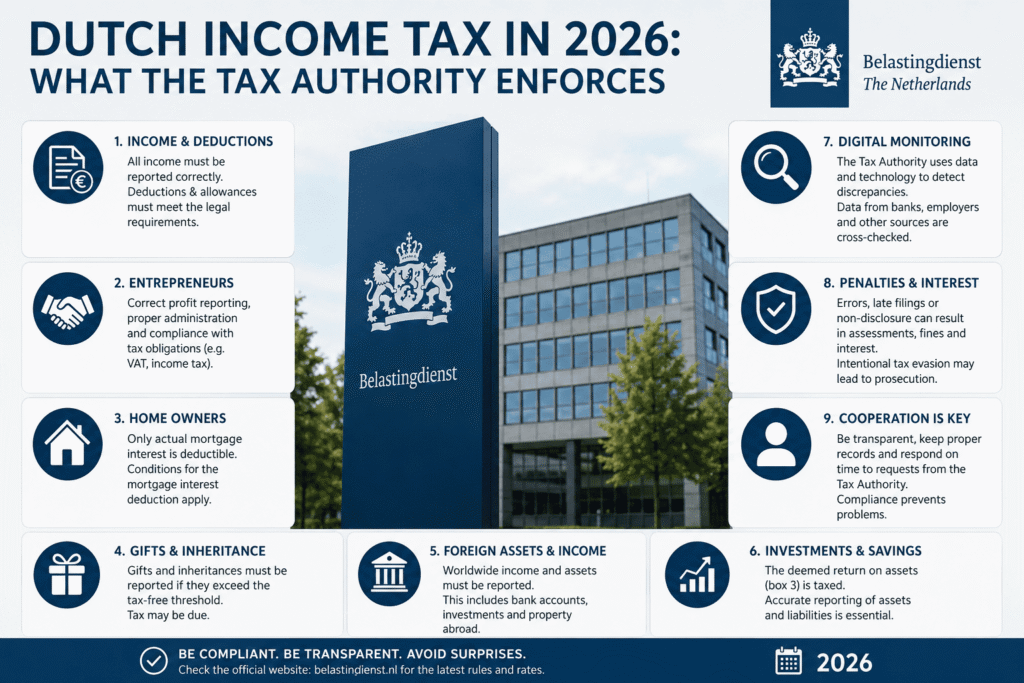

Dutch Income Tax in 2026: What the Tax Authority Enforces

To understand what the Commissioner of Income Tax (Tax Inspector) oversees in the Netherlands, it helps to know how Dutch income tax is structured. The system divides income into three categories, known as Boxes:

Box 1 – Income from Work and Home Ownership

This is the main income category for most residents and expats. It includes salary, freelance income, pensions, and income related to home ownership. In 2026, Box 1 is taxed at:

- 35.75% on income up to €38,883

- 37.56% on income between €38,883 and €78,426

- 49.50% on income above €78,426

Box 2 – Income from Substantial Interest

This applies if you own 5% or more of shares in a company. Dividends and capital gains from such holdings are taxed under Box 2 using a two-tier rate structure.

Box 3 – Savings and Investments

Box 3 covers wealth from savings, investments, and assets. The Dutch system applies a deemed return on your net assets and taxes that assumed return, rather than taxing actual gains directly.

Want to calculate your net salary after Dutch income tax? Use the Dutch Tax Calculator to instantly estimate your take-home pay for 2026 including the impact of the 30% ruling for eligible expats.

Powers of the Dutch Tax Authority (Commissioner of Income Tax Equivalent)

The Belastingdienst Tax Inspector holds several legally defined powers under Dutch tax law:

Power to Request Information

The Tax Inspector can formally demand financial records, bank statements, payroll data, and any other documentation relevant to establishing your tax liability.The Tax Inspector has the power to compulsorily request information from third parties under certain circumstances, including if they believe such information is relevant to determining a taxpayer’s tax liability.

Power to Issue an Information Decree

If a taxpayer believes that certain information does not fall under the disclosure obligation, they can refuse to provide it and wait until the Tax Inspector issues an information decree (informatiebeschikking). Against such a decree, the taxpayer can object and, if the objection is not followed, file an appeal with the appropriate court.

Power to Impose Penalties and Interest

Where underpayment is found whether due to error or deliberate non-compliance the Tax Inspector can add penalty surcharges and collection interest to the outstanding amount.

Power to Extend or Refuse Objection Deadlines

The Tax Inspector manages the formal objection process and can extend the standard decision period when a case requires additional investigation.

Power to Issue Ex Officio Assessments

If no tax return has been submitted, the Inspector will estimate the assessment based on the documents available; this is known as an ex officio assessment and carries the same legal weight as a regular assessment.

How to Dispute a Tax Decision in the Netherlands

If you disagree with a tax assessment issued by the Tax Inspector, the Netherlands provides a structured multi-stage appeal process:

Stage 1 – File an Objection (Bezwaar)

A taxpayer can lodge an objection against a tax assessment with the Dutch tax authorities within six weeks after the date of the tax assessment. Your objection must be submitted in writing either through Mijn Belastingdienst or by post and must explain clearly why you disagree with the assessment.

Stage 2 – Appeal to the District Court (Rechtbank)

If the Tax Inspector’s decision during the objection phase is wholly or partially unfavourable, an appeal can be lodged with the district court (Rechtbank) within six weeks after the date of the decision on the objection.

Stage 3 – Higher Appeal (Gerechtshof)

A notice of appeal can be lodged with the court of appeal (Gerechtshof) within six weeks after the date of the district court’s ruling.

Stage 4 – Supreme Court (Hoge Raad)

An appeal to the Netherlands Supreme Court (Hoge Raad) can be lodged against the decision of the court of appeal within six weeks after the date of the court of appeal’s decision.

Important: If the Tax Administration rejects your objection, you can file an appeal but be aware that you will have to pay tax collection interest on your assessment if the court rejects your appeal. There are also other costs, including court fees and possibly lawyer’s fees.

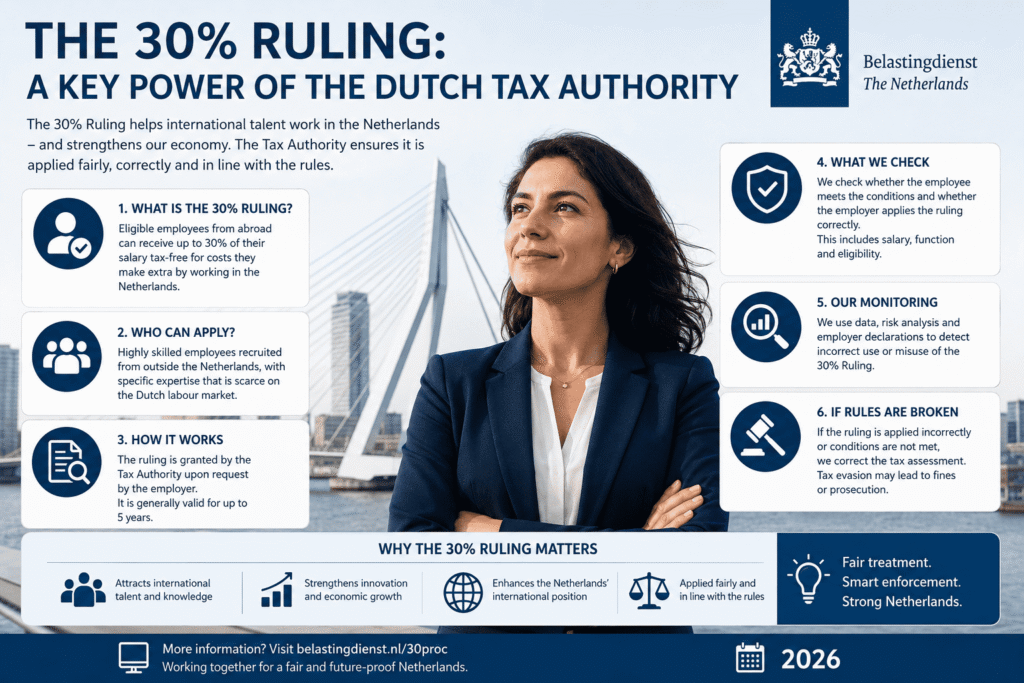

The 30% Ruling: A Key Power of the Dutch Tax Authority

One of the most important decisions the Belastingdienst Tax Inspector makes for expats is the granting or rejection of the 30% ruling (30%-regeling).

The 30% ruling allows qualifying international employees to receive up to 30% of their salary completely tax-free, significantly reducing their Box 1 income tax burden. The Tax Inspector reviews applications for this ruling and decides whether an employee meets the eligibility criteria including the salary threshold, specific expertise requirement, and distance condition.

If your 30% ruling application is rejected or revoked, the same formal objection and appeal process applies as with any other tax decision.

Calculate how the 30% ruling affects your take-home salary: Use the Dutch Tax Calculator to compare your net income with and without the 30% ruling applied.

What Happens During a Dutch Tax Audit?

A tax audit (boekenonderzoek) is one of the most significant interactions a taxpayer can have with the Dutch Commissioner of Income Tax equivalent. Here is what to expect:

Before the audit: The Tax Inspector notifies you in writing of the audit scope and requests relevant documentation typically covering income, deductions, and financial records for one or more tax years.

During the audit: The inspector reviews your records, may conduct an in-person interview, and can request additional documents or explanations. You are legally required to cooperate.

After the audit: If no issues are found, the audit closes without further action. If discrepancies are found, an additional assessment may be issued along with possible penalties. You retain the right to object to any additional assessment within six weeks.

Tips for Staying Compliant with the Dutch Tax Authority

Whether you are an employee, expat, or freelancer in the Netherlands, these steps will help you maintain a clean record with the Belastingdienst:

File your tax return on time. The Dutch income tax return for a given year must be submitted between March and April of the following year. Late filing can trigger fines and automatic assessments.

Keep accurate financial records. The Tax Inspector can audit records going back several years. Maintaining clear documentation of income, deductions, and assets protects you during any review.

Respond to all Belastingdienst communications promptly. Ignoring a tax letter including provisional assessments, information requests, or audit notices can lead to penalties and loss of appeal rights.

Use a tax advisor for complex situations. It is not always easy for individuals, especially foreign ones, to find their way around the Dutch tax system. It might be a good idea to hire the services of a tax consultant or intermediary who can give advice and file tax returns and objections on your behalf.

Check your provisional assessment each year. The Belastingdienst sends a provisional tax assessment (voorlopige aanslag) early in the year. If your income or circumstances have changed, update it promptly through Mijn Belastingdienst to avoid a large year-end settlement.

Frequently Asked Questions (FAQs)

What is the equivalent of a Commissioner of Income Tax in the Netherlands?

In the Netherlands, the role of Commissioner of Income Tax is effectively carried out by the Tax Inspector (belastinginspecteur) of the Belastingdienst. The Tax Inspector assesses income, conducts audits, issues additional tax demands, and decides on formal objections.

Who runs the Dutch Tax Administration (Belastingdienst)?

The Belastingdienst is headed by the Director-General and operates under the Ministry of Finance. It employs over 28,000 staff across regional offices and administers all national taxes in the Netherlands, including income tax, VAT, corporate tax, and customs.

How do I object to a Dutch tax assessment?

You must submit a formal objection (bezwaar) in writing within six weeks of the date on your tax assessment. This can be done through Mijn Belastingdienst online or by post. The Tax Inspector will review your objection and usually issue a decision within six weeks of receipt.

What is an ex officio assessment in the Netherlands?

An ex officio assessment (ambtshalve aanslag) is issued by the Tax Inspector when a taxpayer has not submitted a tax return. The Inspector estimates your tax liability based on available financial data. You can still object to this assessment within six weeks.

Can the Dutch tax authority access my bank account information?

Yes. Under Dutch tax law, the Belastingdienst has the authority to request financial information from banks and third parties when investigating a taxpayer’s income or assets. Banks are legally required to cooperate with such requests.

What is the 30% ruling and who decides on it?

The 30% ruling (30%-regeling) is a tax benefit for qualifying international employees in the Netherlands, allowing up to 30% of their salary to be paid tax-free. The Tax Inspector at the Belastingdienst reviews and approves or rejects applications based on eligibility criteria including salary threshold, specific expertise, and international recruitment conditions.

How long does the Dutch tax dispute process take?

The objection phase usually takes up to six weeks, though the Belastingdienst can extend this period. If you appeal to the district court, the process typically takes several months. Further appeals to the Gerechtshof or Hoge Raad can take one to two years or more.

What happens if I ignore a tax assessment in the Netherlands?

Ignoring a tax assessment means the amount becomes final and collectible. The Belastingdienst can then pursue enforcement action, including collection interest, penalties, and in serious cases, seizure of assets. Always respond to assessments even if you disagree, file a formal objection rather than ignoring the notice.

Is there a statute of limitations on Dutch income tax assessments?

Yes. In general, the Belastingdienst can issue additional assessments for up to five years after the tax year in question. In cases involving fraud or deliberate concealment, this period can be extended to twelve years.

How can I calculate my Dutch income tax for 2026?

The easiest way is to use an online Dutch tax calculator. The Dutch Tax Calculator on dutchtaxcalculators.com provides instant, accurate net salary estimates for 2026 based on your gross income, including options for the 30% ruling, holiday allowance, and different employment types.

Summary

The Commissioner of Income Tax function in the Netherlands is performed by the Tax Inspectors of the Belastingdienst, operating under the Ministry of Finance. These officials hold significant legal authority from assessing income and conducting audits to issuing additional tax demands and ruling on formal objections.

The Dutch tax system operates through a clear, multi-stage dispute process. Taxpayers always have the right to object, appeal, and where necessary escalate to the courts. Understanding how this authority works, what powers it holds, and how to respond to its decisions is essential for anyone living or working in the Netherlands.

Estimate your 2026 Dutch income tax instantly: Use the Dutch Tax Calculator to see your net salary, effective tax rate, and the impact of the 30% ruling all in seconds.

This article is for informational purposes only and does not constitute tax or legal advice. For personalised guidance, consult a registered Dutch tax advisor or the Belastingdienst directly at belastingdienst.nl.

John Keller is a passionate entrepreneur and trusted business advisor dedicated to helping companies grow with clarity, structure, and confidence. With years of experience in business administration, financial management and strategic advisory, he works closely with entrepreneurs to create practical solutions tailored to their unique goals and challenges.

At Look Forward Administratie & Advies, the focus goes beyond numbers and administration. John believes that every successful business starts with clear insight and a strong strategy. By simplifying financial processes and providing real-time business insights, he helps entrepreneurs stay focused on what they do best while building a solid foundation for future growth.

Known for his personal approach and forward-thinking mindset, John supports businesses not only administratively but also as a coach and strategic partner. His mission is to help entrepreneurs recognize opportunities, overcome challenges and achieve long-term success with confidence.