Dutch Inheritance Tax (Erfbelasting) 2026: Complete Guide Rates, Exemptions & How to Pay Less

Introduction: Death and Taxes Even in the Netherlands

The Netherlands has one of the most structured inheritance tax systems in Europe. When someone passes away and leaves behind money, property, or other assets, the people who inherit those assets may need to pay erfbelasting, inheritance tax.

Many people are shocked to discover that a large portion of what they inherit can be taxed, sometimes at rates as high as 40%. But with the right knowledge, many families can significantly reduce or even eliminate their inheritance tax burden.

This guide covers everything you need to know about Dutch inheritance tax in 2026: who pays it, how much, and the smartest legal ways to plan ahead.

What Is Dutch Inheritance Tax (Erfbelasting)?

Erfbelasting is a tax paid by the person who inherits (the heir), not by the estate of the deceased. It is calculated on the net value of what you receive, meaning the total assets minus any outstanding debts of the deceased.

It applies to:

- Cash and bank accounts

- Real estate and property

- Investments and shares

- Business assets

- Valuable personal property (art, jewellery, vehicles)

- Life insurance payouts (in some cases)

The tax is administered by the Belastingdienst (Dutch Tax Authority), and heirs must file a return and pay any tax owed within a specific timeframe.

Who Must Pay Inheritance Tax in the Netherlands?

Dutch inheritance tax applies when the deceased was a Dutch resident at the time of death. If the deceased had moved abroad but had lived in the Netherlands within the 10 years prior to death, Dutch inheritance tax may still apply; this is known as the 10-year rule.

For expats: If you are living in the Netherlands and inherit from a deceased Dutch resident, you may owe Dutch inheritance tax regardless of your own nationality.

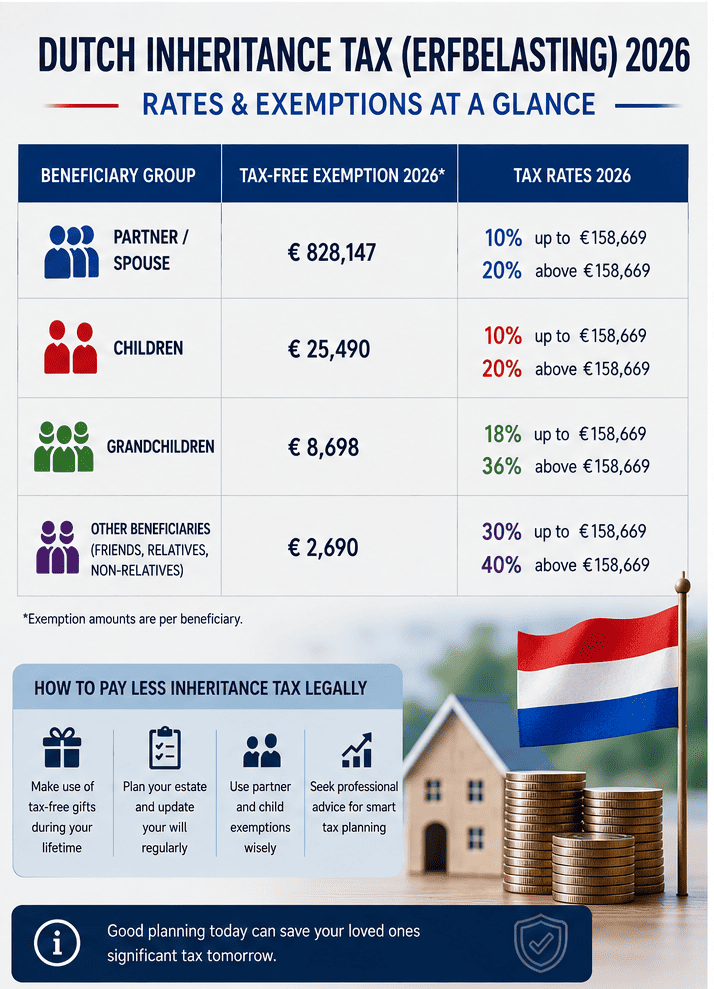

Inheritance Tax-Free Exemptions in 2026

The Netherlands provides generous tax-free exemptions depending on your relationship to the deceased. You only pay tax on the amount above the exemption.

| Relationship to Deceased | Tax-Free Exemption (2026) |

| Spouse / Registered Partner | €795,156 |

| Child or Grandchild | €22,918 |

| Child with a disability (dependent) | €68,751 |

| Parent | €54,270 |

| All other heirs (siblings, friends, etc.) | €2,418 |

Key insight: Partners have an enormous exemption of nearly €800,000, which means most married couples pay zero inheritance tax when one partner passes away.

Inheritance Tax Rates in 2026

For the amount above the tax-free exemption, the following rates apply:

For Partners and Children:

| Taxable Inheritance | Tax Rate |

| Up to €152,368 | 10% |

| Above €152,368 | 20% |

For Grandchildren and Other Descendants:

| Taxable Inheritance | Tax Rate |

| Up to €152,368 | 18% |

| Above €152,368 | 36% |

For All Other Heirs (Siblings, Friends, Non-relatives):

| Taxable Inheritance | Tax Rate |

| Up to €152,368 | 30% |

| Above €152,368 | 40% |

Practical Examples

Example 1: Child Inheriting from a Parent

A parent passes away and leaves €150,000 to their child.

- Tax-free exemption: €22,918

- Taxable amount: €150,000 − €22,918 = €127,082

- Tax owed: 10% × €127,082 = €12,708

- Child receives: €150,000 − €12,708 = €137,292

Example 2: Friend Inheriting

A friend leaves €50,000 in their will to a close friend.

- Tax-free exemption: €2,418

- Taxable amount: €50,000 − €2,418 = €47,582

- Tax owed: 30% × €47,582 = €14,275

- Friend receives: €50,000 − €14,275 = €35,725

This example shows why non-relatives face a very heavy tax burden nearly 30 cents on every euro above the small exemption.

How to File a Dutch Inheritance Tax Return

After someone passes away, heirs must file an aangifte erfbelasting (inheritance tax return) with the Belastingdienst.

Step-by-step process:

- Obtain a BSN (Burgerservicenummer); if you do not already have one, it is required for all tax filings in the Netherlands.

- Determine the net estate value, total assets minus debts of the deceased.

- Calculate each heir’s share based on the will or legal inheritance rules.

- File the return online via Mijn Belastingdienst or by post using paper forms.

- Pay the tax by the deadline stated in the assessment.

Deadline: The inheritance tax return must be filed within 8 months of the date of death. For deaths in 2026, an extension can be requested if needed.

Special Rules and Situations

Inheriting a Family Business (BOR Scheme)

If you inherit a business or company shares, a special relief scheme called the Bedrijfsopvolgingsregeling (BOR) may apply. Under this scheme:

- Up to €1,325,253 of business value is 100% exempt from inheritance tax

- Any amount above this threshold receives a 75% exemption

This makes the Netherlands relatively business-owner friendly when it comes to passing on a company to the next generation. However, the rules are strict, and conditions must be carefully met.

Inheriting a Home (Family Home Exemption)

If a surviving partner inherits the family home, the WOZ value (government-assessed property value) is used for tax purposes, but the partner’s large exemption of €795,156 usually means no tax is owed.

For children inheriting a property, the WOZ value counts toward their €22,918 exemption limit.

Pension and Life Insurance

Most standard Dutch pension rights (AOW, occupational pension) are not subject to inheritance tax, as they cease upon death. However, certain private life insurance payouts or annuity products may be taxable depending on the structure.

Legal Ways to Reduce Dutch Inheritance Tax

Smart estate planning can dramatically reduce or eliminate the inheritance tax your loved ones will pay. Here are proven legal strategies:

1. Make Use of Annual Gift Exemptions During Your Lifetime

Every year, you can give:

- €6,713 tax-free to each child (per parent)

- €2,687 tax-free to others

Over 10 years, a couple can transfer more than €130,000 to each child completely tax-free through annual gifts, reducing the taxable estate significantly.

2. Use the One-Time Enhanced Gift Exemption

Parents can give a child aged 18–40 a one-time tax-free gift of up to €31,813. This directly reduces the future inheritance and lowers the tax bill.

3. Write a Will (Testament)

Without a will, Dutch law determines who inherits (wettelijk erfrecht). A well-structured will can direct assets to heirs with the most favorable tax treatment and ensure your wishes are followed.

4. Consider a Cohabitation Agreement or Partnership Registration

Unmarried cohabiting partners do not automatically receive the spouse exemption of €795,156. Registering a partnership or marrying changes this dramatically.

5. Consult an Estate Planning Professional

For estates above €500,000, professional advice from a notary (notaris) or tax advisor (belastingadviseur) is highly recommended. The savings often far exceed the cost of advice.

Inheritance Tax vs. Gift Tax: A Quick Comparison

| Inheritance Tax (Erfbelasting) | Gift Tax (Schenkbelasting) | |

| When does it apply? | After death | During lifetime |

| Who pays? | The heir | The recipient |

| Partner exemption | €795,156 | N/A |

| Child exemption | €22,918 (annual) | €6,713 per year |

| Filing deadline | 8 months after death | 1 March, the following year |

Strategic lifetime gifting combined with a proper will is the most effective way to reduce the overall tax burden for your family.

Inheritance Tax for Expats: What You Need to Know

Living in the Netherlands as an expat and receiving an inheritance? Here is what matters:

- If the deceased was a Dutch resident, Dutch inheritance tax applies regardless of your nationality.

- If the deceased was a non-resident with no Dutch ties in the past 10 years, Dutch inheritance tax generally does not apply.

- You may face double taxation if both the Netherlands and another country try to tax the same inheritance. The Netherlands has tax treaties with several countries; to avoid this, check if your home country has such a treaty.

- The 30% ruling on your employment income does not affect how inheritance tax is calculated.

Key Numbers at a Glance: 2026 Summary

| Item | Amount |

| Partner/spouse exemption | €795,156 |

| Child/grandchild exemption | €22,918 |

| Disabled dependent child exemption | €68,751 |

| Parent exemption | €54,270 |

| All others exemption | €2,418 |

| Tax rate for children (up to €152,368) | 10% |

| Tax rate for children (above €152,368) | 20% |

| Tax rate for others (up to €152,368) | 30% |

| Tax rate for others (above €152,368) | 40% |

| BOR business relief (up to threshold) | 100% exempt |

| Filing deadline | 8 months after death |

FAQ

What is the inheritance tax exemption for children in 2026?

Each child has a tax-free exemption of €22,918 in 2026. A child with a disability who is financially dependent on the deceased has a higher exemption of €68,751. Any inheritance above these thresholds is subject to tax at 10% (up to €152,368) or 20% (above €152,368).

How much inheritance tax does a friend or sibling pay in 2026?

Friends, siblings, and non-relatives have a very small exemption of only €2,418. On the amount above this, they pay 30% up to €152,368 and 40% on anything above it. For example, a friend inheriting €50,000 pays approximately €14,275 in tax — keeping only €35,725.

How much is the tax-free exemption for a partner or spouse in 2026?

A surviving spouse or registered partner has a tax-free exemption of €795,156 in 2026. This is the largest exemption available, meaning most married couples pay zero inheritance tax when one partner passes away. Only the amount above this threshold is taxed.

Does the 30% ruling affect my pension tax?

No. The 30% ruling only applies to employment income during your working years in the Netherlands. It does not apply to pension income. Once you retire, full Dutch income tax rules apply to all your pension payments regardless of whether you previously benefited from the 30% ruling.

Conclusion: Plan Early, Pay Less

Dutch inheritance tax is a reality that affects many families, especially those with significant assets, property, or business interests. The good news is that the Netherlands provides generous exemptions for partners and children, and with careful planning, the tax burden can be substantially reduced.

The most powerful tools are simple: make regular use of annual gift exemptions, write a clear will, and ensure unmarried partners have legal protection through partnership registration.

If your estate is significant, professional estate planning is one of the best investments you can make, not for yourself but for the people you love.

Disclaimer: This blog is for informational purposes only and does not constitute legal, financial, or tax advice. Inheritance tax rules are subject to change. Always consult a qualified Dutch notary or tax advisor for personalized guidance on your situation.

Related Articles on DutchTaxCalculators.com:

John Keller is a passionate entrepreneur and trusted business advisor dedicated to helping companies grow with clarity, structure, and confidence. With years of experience in business administration, financial management and strategic advisory, he works closely with entrepreneurs to create practical solutions tailored to their unique goals and challenges.

At Look Forward Administratie & Advies, the focus goes beyond numbers and administration. John believes that every successful business starts with clear insight and a strong strategy. By simplifying financial processes and providing real-time business insights, he helps entrepreneurs stay focused on what they do best while building a solid foundation for future growth.

Known for his personal approach and forward-thinking mindset, John supports businesses not only administratively but also as a coach and strategic partner. His mission is to help entrepreneurs recognize opportunities, overcome challenges and achieve long-term success with confidence.